Rockets and Returns: Why Procuring Launch Is Like Investing

In the newspace economy, launch isn’t logistics, it’s capital allocation.

In my last piece, I broke down the technical and strategic variables behind launch; why not all launch vehicles are created equal, and why that matters more than most people think.

But knowing what kind of rocket to choose is only half the story.

The other half?

Knowing how and when to buy it.

Because in space, launch procurement isn’t just a logistical decision. It’s a form of capital deployment.

And the smartest customers don’t just act like buyers, they act like investors.

Launch Is Not a Commodity. It’s a Bet.

There’s a misconception especially outside the space sector that launch is like booking a flight. Pick a provider, pay a price, get a ride.

But rockets aren’t taxis.

They aren’t interchangeable. They aren’t on-demand. And they certainly don’t come with instant refunds.

When you procure launch, especially in a fragmented, evolving, and capacity-constrained market, you’re not just securing a payload delivery. You’re placing a time-sensitive, risk-weighted bet on a company’s ability to deliver when it matters most.

It’s not just a transaction. It’s portfolio strategy.

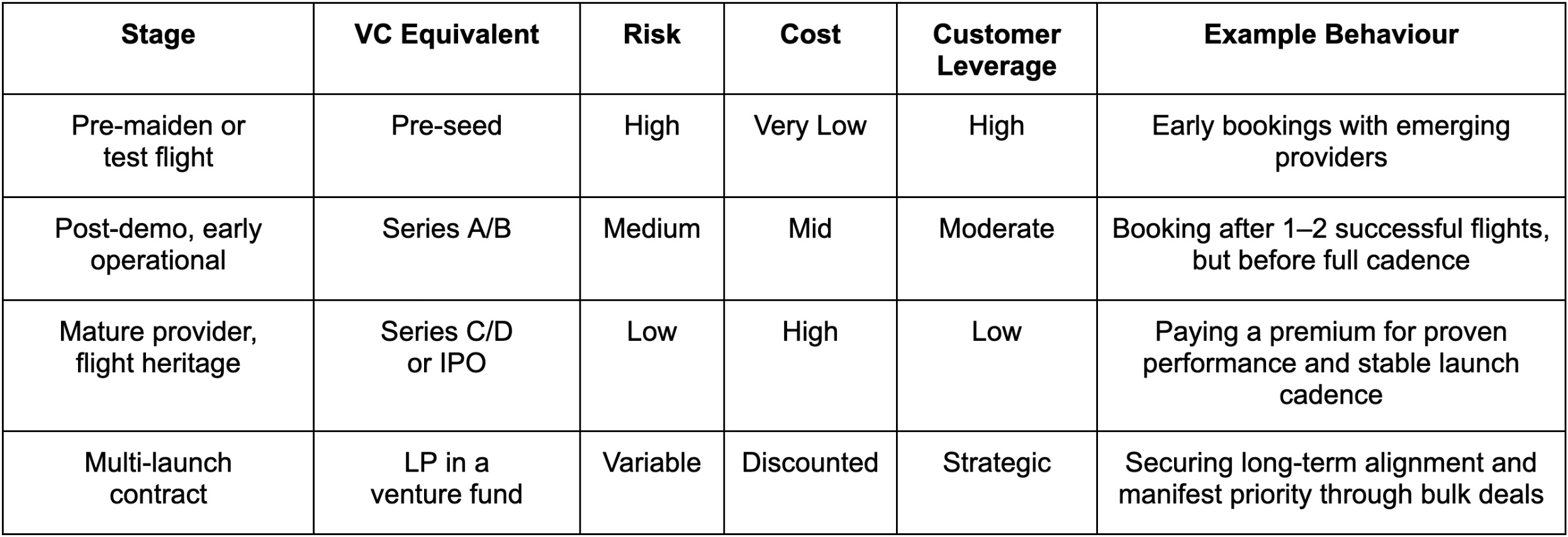

The VC Analogy: When You Procure Launch, You’re Buying Stage Exposure

Just like investors choose to enter at pre-seed, Series A, or post-IPO depending on risk appetite, launch customers choose between early-stage and mature providers. Each comes with a different profile of cost, confidence, and control.

Launch procurement mirrors startup investing. Here’s the model:

Early customers get lower pricing and deeper influence, but take on greater uncertainty. Later-stage customers pay more for reliability, heritage, and a seat at the back of the queue that’s often prioritised for institutional clients.

For example:

Planet and ICEYE, during their early growth phases, booked rides with emerging providers like Rocket Lab well before these providers had demonstrated consistent flight cadence. This approach granted them priority access, bespoke integration, and cost advantages, at the expense of accepting potential launch delays and technical risk.

In contrast, newer operators entering the market now face fewer provider options and often find themselves queued behind large customers on mature launchers like SpaceX. This typically means compromising on orbital specifics or settling for later launch slots.

Meanwhile, Spire Global has taken a more portfolio-driven approach, flying with Arianespace, SpaceX, Rocket Lab, ISRO, and JAXA. This mixed strategy has enabled Spire to hedge against schedule disruptions, align different launch types to mission-specific needs, and avoid dependency on any single provider or regulatory environment.

It’s the same tradeoff investors face every day: Enter early and shape the trajectory, or enter late and accept the terms.

Timing the Market: The Smart Buyer’s Edge

One of the most persistent misconceptions in satellite planning is:

“We’ll book the launch when the satellite is ready.”

But launch timelines don’t align with payload readiness. They align with manifests, and manifests fill fast.

Launch is not a just-in-time service. It’s a constrained pipeline shaped by vehicle production cycles, regulatory windows, range availability, and integration bottlenecks. Providers often book out 12 to 36 months in advance, especially on high-demand routes like Sun-Synchronous Orbit (SSO) or for rideshare launches on vehicles like Falcon 9.

If your mission is scheduled for 2027, your procurement window isn’t in 2026; it’s right now.

The most strategic customers don’t react to readiness. They forecast availability, anticipate constraints, and secure slots early, sometimes before the payload is even off the drawing board.

It’s the same logic investors apply to capital markets: You don’t wait for the IPO. You invest at the inflection point when the upside is highest, and access is still possible.

Your Payload’s Orbit Is an Investment Thesis

If you’re deploying multiple satellites, building constellations, or planning long-term orbital infrastructure, you’re not making a one-time procurement decision.

You’re managing a portfolio of launch exposures.

Smart operators hedge launch risk the same way investors hedge capital risk:

Mixing dedicated and rideshare to balance control, timing, and cost

Blending heritage providers with emerging launchers to diversify reliability against flexibility and price

Geographically diversifying launch sites to mitigate regulatory constraints (e.g., ITAR) and reduce geopolitical exposure

This isn’t about securing the lowest cost per kilogram. It’s about maximising mission continuity, building schedule resilience, and preserving strategic optionality in a fast-evolving launch ecosystem.

Relationship Capital: The Unseen ROI

In early-stage investing, soft capital matters: access, alignment, and founder trust. In launch, relationship capital is just as important.

Early adopters often enjoy:

Co-creation influence: Input on vehicle development or payload interfaces

Flexible integration: Custom windows, site-specific preferences, additional test cycles

Priority access: Better manifest positioning, deeper engineering support

Take Rocket Lab again. Their earliest customers, many of whom flew academic or climate missions, became anchor clients, securing long-term launch arrangements that now reap dividends in speed, support, and roadmap integration.

The lesson? Trust compounds. So does loyalty.

The more a launcher knows your platform, the better the results and the faster you move.

Vertical Integration: Owning the Launch Stack

In the increasingly crowded launch market, not all providers are created equal. While some players rely on fragmented supply chains and third-party integration, others are bringing everything under one roof: building engines, tanks, avionics, GSE, and software in-house.

This vertically integrated model is more than just a manufacturing philosophy. It’s a strategic differentiator.

Take PLD Space as a case in point. The company designs, builds, tests, and integrates its launch vehicles entirely in Spain. This model offers several key advantages:

Reduced supplier risk and greater control over schedule

Faster design-to-test iterations, enabling rapid improvement

Clearer export classification and sovereign independence

Stronger IP protection and quality assurance

This stands in contrast to providers that rely heavily on subcontractors, sometimes across multiple jurisdictions, introducing complexity, coordination delays, and export control regulation bottlenecks.

For customers, a vertically integrated provider can offer greater schedule reliability, more responsive engineering support, and fewer surprises in integration. In a procurement context, that can mean the difference between a seamless mission and a six-month delay.

Just as investors prefer startups with deep in-house technical capability, launch customers increasingly look for providers with tight internal loops, clean supply chains, and end-to-end control.

Launch Insurance as a Service Layer

In a high-stakes domain like launch, insurance isn’t just a post-procurement checkbox. It’s increasingly becoming part of the provider’s value proposition.

Traditionally, satellite operators worked with third-party brokers to underwrite launch and in-orbit risk. But a growing number of launch companies are facilitating insurance, either by partnering with preferred underwriters or offering bundled service packages that simplify access to coverage. This trend is blurring the line between technical provider and mission risk advisor, especially for smallsat operators navigating complex insurance markets for the first time.

This shift is strategic.

For customers, especially first-time or small operators, navigating the insurance market can be opaque and expensive. By connecting customers directly to carriers or including add-ons in a package, launch providers reduce friction, simplify deal flow, and signal confidence in their own reliability.

Emerging players like PLD Space with growing flight heritage are well-positioned to adopt similar models, especially as flight heritage builds and sovereign customers seek integrated, secure solutions. For a customer booking launch from a vertically integrated provider that controls its supply chain, range, and QA processes, a bundled insurance offering becomes both credible and attractive.

From the provider’s side, facilitating insurance isn’t just about customer support. It’s a form of signal amplification:

“We’re confident enough in our vehicle to put insurance on the table.”

In a competitive landscape where newspace launchers are fighting to build trust, offering insurance isn’t just a service; it’s strategy.

A Safety Net in Orbit: The Role of Relaunch Guarantees

In the high-stakes world of launch, even with rigorous testing, failures can happen. That’s where relaunch guarantees come in.

A relaunch guarantee is a contractual commitment by the launch provider to offer a replacement launch at no additional cost, or at a significantly reduced rate, if the initial mission fails due to issues on their end.

It’s not the same as traditional insurance. Rather than compensating with cash, the provider compensates with another shot at orbit.

This is especially valuable for:

Small satellite operators who can’t afford double insurance premiums

Early-stage missions where budget constraints are tight

Institutional users who need continuity more than cash reimbursement

Some providers offer this guarantee directly; others bundle it with insurance packages through underwriters.

In an environment where flight heritage is still being built, relaunch guarantees are emerging as a trust-building mechanism, offering reassurance, risk mitigation, and competitive differentiation all at once.

Launch Is Not Just Transport. It’s Infrastructure

Venture capitalists don’t get excited about consumer-facing features.

They get excited about infrastructure: the underlying scaffolding that makes economies move.

Launch is that scaffolding.

It is not the end product. It is the enabler of entire markets downstream: Earth observation, climate intelligence, broadband constellations, and sovereign space capabilities. In a functioning space economy, launch is the first critical layer of value creation.

Your mission may start with a rocket, but the real return is found in:

Delivering high-resolution, real-time data

Building scalable orbital business models

Establishing national security and technological sovereignty

Launch is your seed round.

Orbit is Series A.

Impact is the exit.

In this framing, launch isn’t just access, it’s positioning. And how you position determines what returns you’re capable of generating.

Final Thought: The Smartest Mission Managers Think Like Capital Allocators

If you’re a satellite operator, mission director, or policymaker, stop thinking of launch as a line item.

Start thinking like a capital allocator.

Because launch isn’t just logistics. It’s a strategic bet on readiness, resilience, and returns.

The best operators don’t just procure launches. They position themselves:

To minimise timing risk

To diversify across geographies and providers

To build trust and integration advantages over time

They manage their launch roadmap like a portfolio, with asymmetric upside for those who bet early, and compounding value for those who play the long game.

So the next time someone says, “We just need a launch provider,” ask them this instead:

What are you really investing in? And what returns are you expecting?

Because in space, how you get there shapes everything that follows.

And in a capacity-constrained, capital-intensive ecosystem like this one, the smartest customers aren’t just booking rockets. They’re buying future market position.